EN

EN

AR

AR

BG

BG

FR

FR

DE

DE

HI

HI

IT

IT

JA

JA

KO

KO

PT

PT

RO

RO

RU

RU

ES

ES

TL

TL

IW

IW

ID

ID

LV

LV

LT

LT

SR

SR

SK

SK

SL

SL

UK

UK

VI

VI

SQ

SQ

GL

GL

HU

HU

MT

MT

TH

TH

TR

TR

AF

AF

GA

GA

BE

BE

MK

MK

HY

HY

AZ

AZ

KA

KA

BN

BN

BS

BS

LO

LO

MN

MN

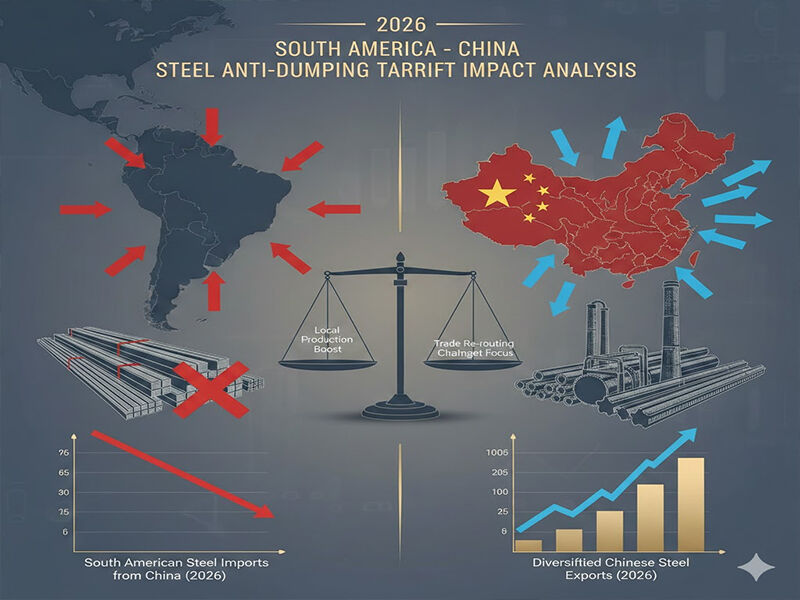

ໃນປີ 2026, ສະຖານະການໄດ້ປ່ຽນແປງຕະຫຼາດເຫຼັກໃນອາເມລິກາໃຕ້ຢ່າງເລິກເຊິ່ງ ເນື່ອງຈາກສະບຽບການການຈັດເກັບຄ່າທຳນຽມຕໍ່ການຂາຍສິນຄ້າລາຄາຖືກ (antidumping regulations) ຕໍ່ຜະລິດຕະພັນເຫຼັກຈີນ ໄດ້ເພີ່ມຂຶ້ນເຖິງຈຸດສູງສຸດໃນປະຫວັດສາດ. ອຸປະສັກດ້ານອາກອນໄດ້ຖືກປະຕິບັດຢ່າງເປັນເອກະພາບຕາມຮູບແບບຂອງຜະລິດຕະພັນ ເຊິ່ງເປັນສ່ວນໃຫຍ່ຂອງກິດຈະການຂອງບໍລິສັດຕ່າງໆ ເຊັ່ນ: Shandong Runhai Stainless Steel Co., Ltd. ບຣາຊິວ, ອາເຈນຕິນາ ແລະ ໂຄລົມເບຍ ທີ່ນຳເຂົ້າເຫຼັກຫຼາຍກວ່າ 80 ເປີເຊັນຂອງເຫຼັກທັງໝົດໃນເຂດດັ່ງກ່າວ. ມາດຕະການດັ່ງກ່າວ ທີ່ມີອັດຕາອາກອນສະເລ່ຍ 35-50 ເປີເຊັນຕໍ່ມູນຄ່າສິນຄ້າ (ad valorem) ໄດ້ປະສົມປະສານເທົ່າທຽມກັນໃນດ້ານການແຂ່ງຂັນຂອງຜູ້ສົ່ງອອກເຫຼັກຈີນ ແລະ ໄດ້ບັງຄັບໃຫ້ເຂົາເຈົ້າຕ້ອງທົບທວນຄືນວິທີການຂອງຕົນຕໍ່ຕະຫຼາດອາເມລິກາໃຕ້.

ຜະລິດຕະພັນແບບແຕ່ງແທນ (Flat Products) ຢູ່ໃຕ້ຄວາມກົດດັນ

ການສືບສວນທີ່ດຳເນີນການຕໍ່ການຂາຍສິນຄ້າໃນລາຄາຕ່ຳກວ່າມູນຄ່າ (antidumping) ໄດ້ໃຫ້ຄວາມສຳຄັນຢ່າງຫຼາຍຕໍ່ຜະລິດຕະພັນທີ່ຖືກມວນເປັນແຜ່ນ (flat-rolled products) ເຊິ່ງເປັນຜະລິດຕະພັນຫຼັກໃນປະເທດທີ່ສົ່ງອອກຂອງ Shandong Runhai. ການຫ້າມທີ່ເຂັ້ມງວດທີ່ສຸດປະກອບດ້ວຍແຜ່ນເຫຼັກສະແຕນເລດ ແລະ ແຜ່ນມວນ, ຜະລິດຕະພັນເຫຼັກທີ່ຖືກຊຸບສັງกะສີ ແລະ ແຜ່ນມວນທີ່ຜະລິດຈາກ PPGI/PPGL. ໃນປີ 2026 ບຣາຊິວໄດ້ກຳນົດອາກອນຕໍ່ເຫຼັກສະແຕນເລດທີ່ຖືກມວນເຢັນຈາກຈີນ ເທົ່າກັບ $485.73 ຕໍ່ຕັນ, ເຊິ່ງເຮັດໃຫ້ຂໍ້ໄດ້ປຽບດ້ານລາຄາທີ່ເປັນເຫດຜົນໃຫ້ການຂະຫຍາຍຕົວເຖິງ 40% ຕໍ່ປີໃນເສັ້ນທາງນີ້ໃນປີ 2025 ສິ້ນສຸດລົງຢ່າງມີປະສິດທິຜົນ.

ອາກອນລວມ ເຖິງ ແຜ່ນເຫຼັກທີ່ຖືກຊຸບສັງກະສີ ແລະ ແຜ່ນມວນ (ທີ່ຕ້ອງການໃນການກໍ່ສ້າງ ແລະ ໃຊ້ໃນອຸດສາຫະກຳລົດ) ໄດ້ເພີ່ມຂຶ້ນເຖິງຫຼາຍກວ່າ 55% ໃນຕະຫຼາດໃຫຍ່ໆເຫຼັ່ນ: ໂຄລົມເບຍ ແລະ ອາເຈນຕິນາ. ລາຄາທີ່ເຂົ້າເຖິງຈຸດປະສົງ (landed cost) ຂອງຕູ້ຂົນສົ່ງ 20 ໄຟ (feet) ທີ່ບັນຈຸແຜ່ນມວນທີ່ຖືກຊຸບສັງກະສີ ດ້ວຍລາຄາສະເລ່ຍ $25,000 FOB Qingdao ໃນລາຄາປັດຈຸບັນທີ່ບຸເອໂນສໄອລີສ ມີມູນຄ່າເຖິງຫຼາຍກວ່າ $38,750 ແລະ ສິ່ງນີ້ເຮັດໃຫ້ສິນຄ້າຈີນບໍ່ສາມາດເຂົ້າເຖິງໄດ້ສຳລັບຜູ້ຊື້ໃນອາເມລິກາໃຕ້ ຜູ້ທີ່ມີຄວາມອ່ອນໄຫວຕໍ່ລາຄາ.

ຜະລິດຕະພັນຍາວ ແລະ ວັດຖຸສຳລັບສິ່ງອຳນວຍຄວາມສະດວກພື້ນຖານ

ມັນບໍ່ໄດ້ຖືກປ້ອງກັນຈາກຜະລິດຕະພັນຍາວເຫຼົ່ານີ້ເຊັ່ນ: ຄີມ H&I , ແຖບມຸມ ແລະ ຊ່ອງ U&C ເຊິ່ງເປັນທີ່ນິຍົມໃນອຸດສາຫະກຳພື້ນຖານທີ່ກຳລັງຂະຫຍາຍຕัวຢູ່ໃນອາເມລິກາໃຕ້. ໃນຕົ້ນປີ 2026 ປະເທດເປີູ ແລະ ໄຊລີ ໄດ້ກຳນົດອັດຕາຄ່າທັນທີທັນໃດຕໍ່ເຫຼັກໂຄງສ້າງຈີນໃນອັດຕາ 28 ຫາ 42 ເປີເຊັນ ໂດຍອ้างວ່າສິນຄ້າເຫຼັກດັ່ງກ່າວກຳລັງເຮັດຮ້າຍຕໍ່ຜູ້ຜະລິດທ້ອງຖິ່ນ. ສິ່ງດຽວກັນນີ້ກໍສາມາດເວົ້າໄດ້ກ່ຽວກັບເຫຼັກແຖບປັກ, ທໍ່ເຫຼັກລາດທີ່ມີຄວາມຫຼາຍ (ductile iron pipes), ແລະ ເຫຼັກເສັ້ນທີ່ມີຮູບຮ່າງບິດ (deformed steel bars) ເຊິ່ງເປັນອົງປະກອບສຳຄັນຂອງໂຄງການກໍ່ສ້າງທ່າເຮືອ ແລະ ໂຄງການພື້ນຖານດ້ານນ້ຳ; ຂໍ້ມູນຈາກສາງສິນຄ້າທີ່ຖືກຈັດເກັບໄວ້ (bonded warehouse) ແຕ່ເປີດເຜີຍວ່າສິນຄ້າທີ່ມີຄວາມຍາວ (long product inventories) ຈາກຈີນໄດ້ຫຼຸດລົງ 63% ໃນທ່າເຮືອຂອງອາເມລິກາໃຕ້.

ຜະລິດຕະພັນທີ່ມີການປູກແລະຜະລິດຕະພັນພິເສດ

ເຫດການນີ້ໄດ້ສົ່ງຜົນຮ້າຍຢ່າງຮຸນແຮງຕໍ່ສ່ວນຂອງເຫຼັກທີ່ມີການປູກ (coated steel section) ເຊິ່ງປະກອບດ້ວຍແຜ່ນຫຼັງຄາ ແລະ ຜະລິດຕະພັນທີ່ມີສີທີ່ຖືກປູກ. ເຊິ່ງຜູ້ຜະລິດຈີນໄດ້ສ້າງຕັ້ງພື້ນທີ່ຕະຫຼາດທີ່ເຂັ້ມແຂງ. ຄຳສັ່ງກ່ຽວກັບການນຳໃຊ້ການທັນທີທັນໃດ Ppgi coils ໃນປະເທດບຣາຊິນ, ເຊິ່ງຈະສໍາເລັດໃນເດືອນກຸມພາ 2026, ຈະວາງຄ່າທໍານຽມ 628.34 ຕໍ່ໂຕນທີ່ກວ້າງທີ່ສຸດໃນການກໍ່ສ້າງເຮືອນ. ນີ້ແມ່ນການເພີ່ມຂຶ້ນ 110 ເປີເຊັນ ຂອງລາຄາທີ່ປົກກະຕິໃນປີ 2025 ທີ່ເຮັດໃຫ້ການສັ່ງຊື້ໃຫມ່ຢຸດເຊົາ. ເຫຼັກຊິລິໂຄນ , ຊຶ່ງເປັນຜະລິດຕະພັນທີ່ສໍາຄັນໃນການຜະລິດຂອງ transformers ໄຟຟ້າແລະການສົ່ງອອກທີ່ໄດ້ເພີ່ມຂຶ້ນເປັນສ່ວນໃຫຍ່ຂອງຈີນ ການສົ່ງອອກຂອງໂຮງງານຜະລິດໄຟຟ້າ ແມ່ນໄດ້ຮັບຜົນກະທົບຈາກການເກັບພາສີຕ້ານການນໍາພາ 32,5% ທີ່ຖືກວາງຂຶ້ນໂດຍປະເທດອາເຈນຕິນາ ແລະໄດ້ສົ່ງຜົນກະທົບຕໍ່ລະບົບຕ່ອງໂສ້ການສະຫນອງຂອງອຸດສາຫະກໍາພະລັງງານທົດແທນທີ່ເພີ່ມຂຶ້ນໃນພາກພື້ນ.

ຜົນກະທົບທາງດ້ານຍຸດທະສາດ ສໍາ ລັບຜູ້ສົ່ງອອກຈີນ

ຜູ້ສະ ຫນອງ ທີ່ຫຼາກຫຼາຍເຊັ່ນ Shandong Runhai ທີ່ຂາຍສາຍຜະລິດຕະພັນທີ່ກວມເອົາເກືອບທັງ ຫມົດ ຂອງສາຍຜະລິດຕະພັນທີ່ໄດ້ຮັບຜົນກະທົບ, ລວມທັງທໍ່ເຫຼັກກ້າທີ່ບໍ່ມີທາດເຫຼັກເຖິງທໍ່ທອງແດງ, ແຜ່ນອະລູມິເນີ້ມ ການປັບປຸງສະພາບແວດລ້ອມການຕ້ານການຄ້າ 2026 ຈະຕ້ອງມີການປ່ຽນແປງທາງດ້ານຍຸດທະສາດຢ່າງຫນັກ. ການສືບສວນຕະຫຼາດສະແດງໃຫ້ເຫັນວ່າ ຜູ້ຊື້ອາເມລິກາໃຕ້ ກໍາ ລັງແບ່ງແຍກຢ່າງຕັ້ງຫນ້າ ລະບົບການສະຫນອງຂອງເຂົາເຈົ້າ ນອກຈາກຈີນ , ແລະ ຈຸດປະສົງອື່ນໆທີ່ເປັນໄປໄດ້ສຳລັບການຈັດຊື້ແມ່ນ ເວຍຕົນນາມ, ເກົາຫຼີໃຕ້, ແລະ ເມັກຊິໂກ.

ຢ່າງໃດກໍຕາມ, ຍັງມີທີ່ຫວ່າງໃນການຄົ້ນຫາ. ຫົວໝາກ_nickel ແລະ ບາງຜະລິດຕະພັນພິເສດ ເຫຼັກສະຕາເລດທີ່ບໍ່ເກີດຂຶ້ນຈາກການລົ້ມລະລາຍໄດ້ຮັບການປະເຊີນກັບຄວາມກົດດັນຈາກການຕໍ່ຕ້ານການລົ້ມລະລາຍໂດຍກົງ ແລະ ສິ່ງນີ້ຊີ້ໃຫ້ເຫັນເຖິງຄວາມເປັນໄປໄດ້ທີ່ຈະເຄື່ອນໄປສູ່ຜະລິດຕະພັນທີ່ມີຄວາມແຕກຕ່າງດ້ານເຕັກນິກຫຼາຍຂຶ້ນ ແລະ ມີມູນຄ່າສູງ. ບໍລິສັດດັ່ງກ່າວຍັງເຄີຍມີຄວາມສຳພັນກັບບໍລິສັດເຫຼັກທ້ອງຖິ່ນທີ່ໃຫຍ່ທີ່ສຸດເຊັ່ນ: Shandong Iron and Steel ແລະ Tangshan Iron and Steel ທີ່ຈະຊ່ວຍໃຫ້ບໍລິສັດນີ້ສາມາດຈັດສົ່ງປະລິມານນ້ອຍໆໄປຍັງຕະຫຼາດທີ່ບໍ່ໄດ້ຢູ່ໃນອາເມລິກາໃຕ້ ແຕ່ຍັງເຂົ້າເຖິງໄດ້.

ອັດຕາສະບາຍການຕໍ່ຕ້ານການລົ້ມລະລາຍປີ 2026 ບໍ່ແມ່ນການເຄື່ອນໄຫວດ້ານການຄ້າທີ່ຊົ່ວຄາວ ແຕ່ເປັນການປ່ຽນແປງຢ່າງຮຸນແຮງຕໍ່ການຈັດຊື້ເຫຼັກໃນອາເມລິກາໃຕ້ . ຜູ້ສົ່ງອອກເຫຼັກຈາກຈີນບໍ່ຢູ່ໃນຍຸກທີ່ເປັນການເຂົ້າສູ່ຕະຫຼາດດ້ວຍປະລິມານອີກຕໍ່ໄປ. ເພື່ອຈະສາມາດປະສົບຜົນສຳເລັດໃນສະຖານະການປັດຈຸບັນ, ພວກເຂົາຈຳເປັນຕ້ອງມີການຊີ້ນຳດ້ານຜະລິດຕະພັນ, ການປຸງແຕ່ງເພີ່ມມູນຄ່າ, ແລະ ການແຈກຢາຍຕະຫຼາດຢ່າງເປັນຢ່າງຍຸດທະສາດ. ບໍລິສັດທີ່ສາມາດຈັດການໃນສະພາບແວດລ້ອມທີ່ທ້າທາຍນີ້ ເຊັ່ນ: Shandong Runhai ແມ່ນບໍລິສັດທີ່ມີການຈັດການສິນຄ້າເຂົ້າສະຕັອກຢ່າງດີ ແລະ ມີຫຼາຍຊ່ອງທາງການຈັດສົ່ງໃນລະດັບປະເທດ. ຄວາມຄິດທີ່ໄດ້ຮັບການຍອມຮັບວ່າເປັນການຮ່ວມມືທີ່ທັງສອງຝ່າຍໄດ້ຮັບປະໂຫຍດ ເຊິ່ງໄດ້ເປັນຄວາມຄິດທີ່ຊີ້ນຳໃນການພັດທະນາຂອງພວກເຂົາ ຈະຕ້ອງຖືກຖ່າຍໂອນໄປສູ່ຕະຫຼາດໃໝ່ ແລະ ການພັດທະນາຜະລິດຕະພັນທີ່ຈະບໍ່ຢູ່ຕໍ່າກວ່າກຸ່ມສິນຄ້າທີ່ກຳລັງປະເຊີນກັບອຸປະສັກດ້ານການຄ້າໃນອາເມລິກາໃຕ້.